Research

Publications

1. Stablecoin Devaluation Risk (2025)

European Journal of Finance

(with Barry Eichengreen and Ganesh Viswanath-Natraj)

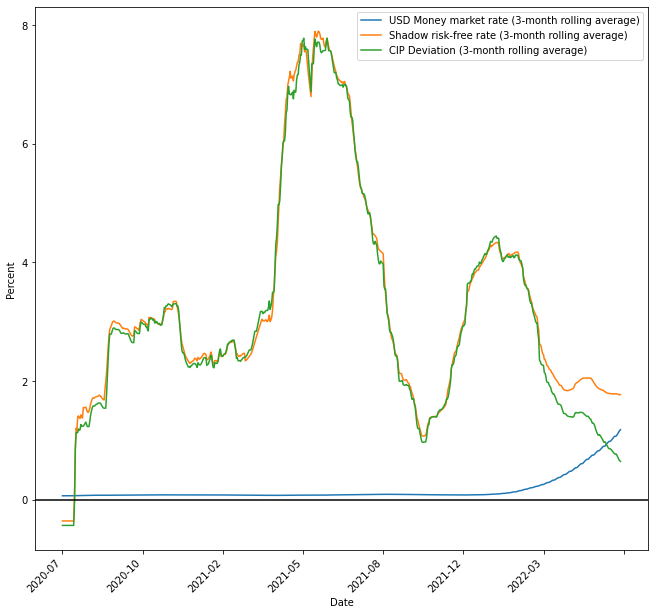

Abstract: We construct market-based measures of stablecoin devaluation risk using spot and futures prices for Tether. We estimate an average probability of devaluation over one year of 60 basis points, rising to 200 basis points during the March 2020 ‘Black Thursday’ Crypto crash and the March 2022 Terra-Luna crash. One might expect devaluation probabilities to be connected to interest rates on stablecoins at DeFi lending protocols via covered interest parity; contrary to this expectation, we find that deviations from covered interest parity are pervasive. Nor do stablecoin interest rates respond to Federal Reserve policy announcements in the manner of conventional market interest rates. We suggest explanations for these disconnects, including market segmentation, lack of term structure in DeFi interest rates, lack of arbitrage capital in cryptocurrency markets, and transaction costs of arbitrage.

Presentations: Global AI Finance Research Conference (Ho Chi Minh City) 2023, Tokenomics at Columbia University 2023 (New York), MARBLE* 2023 (London)

A video of me presenting the paper at the Tokenomics Conference at Columbia Business School!!!

2. Signal in the Noise: Trump Tweets and the Currency Market (2025)

Journal of International Money and Finance

(with Ilias Filippou, Arie E. Gozluklu, and Ganesh Viswanath-Natraj)

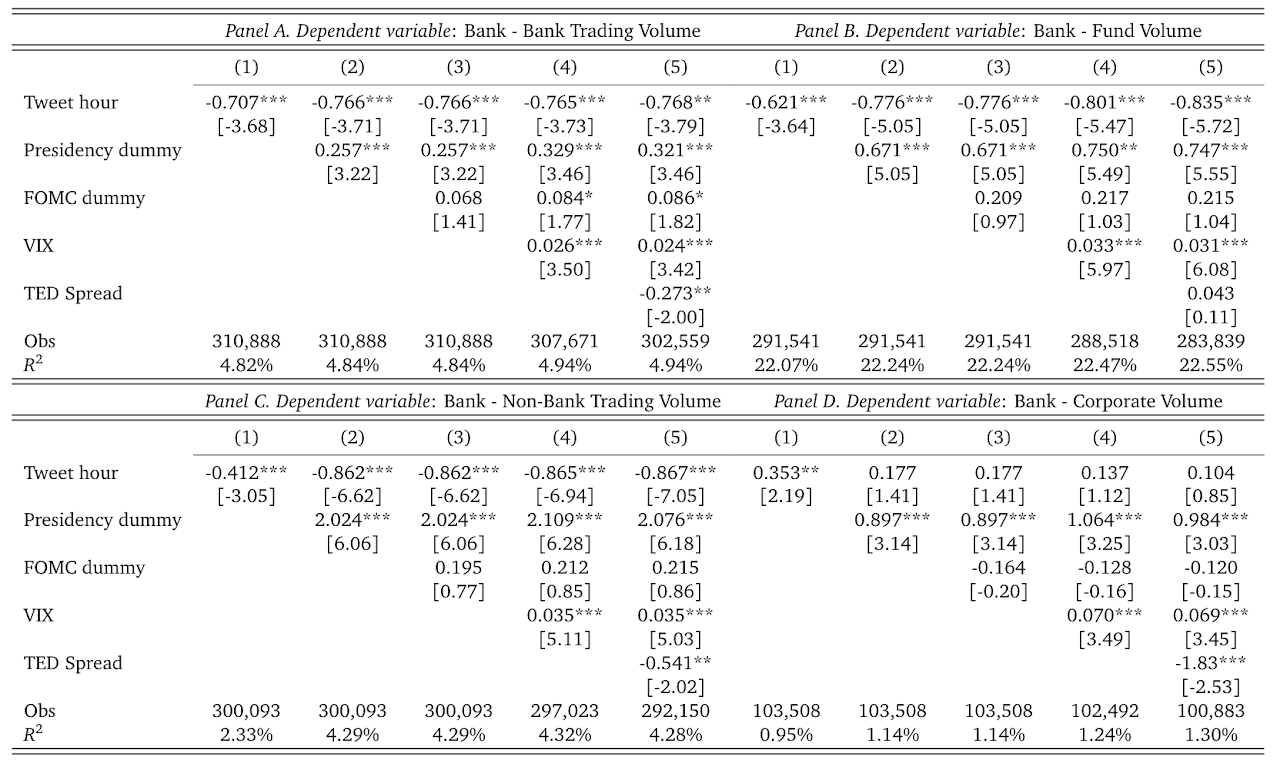

Abstract: Using textual analysis, we identify the set of Trump tweets that contain information on macroeconomic policy, trade or exchange rate content. We then analyse the effects of Trump tweets on the intraday trading activity of foreign exchange markets, such as trading volume, volatility and FX spot returns. We find that Trump tweets reduce speculative trading, with a corresponding decline in trading volume and volatility, and induce a bias reflecting Trump’s (optimistic) views on the U.S. economy. We rationalise these results within a model of Trump tweets revealing economic content as a public signal that reduces disagreement among speculators.

Presentations: Finance Forum* 2022, AFA PhD Poster Session 2022 (Boston, virtual meeting), Queen Mary Behavioural Finance Seminar 2022 (London), 37th International Conference of the French Finance Association 2021 (Paris, virtual meeting), 34th Australasian Finance and Banking Conference 2021 (Sydney, virtual meeting), Warwick Business School Brown Bag 2020 (Warwick).

3. Investor Attention to News on Financial Integration and Currency Returns (2024)

Handbook of Financial Integration, Edward Elgar Publishing (EEP), chapter 3

(with Ilias Filippou and Mark P. Taylor)

4. Regional economic sentiment: Constructing quantitative estimates from the Beige Book and testing their ability to forecast recessions

Economic Commentary, Federal Reserve Bank of Cleveland, no. 2024-08 (April)

(with Christian Garciga, Ilias Filippou and James Mitchell)

Working papers

1. Fundamental Sentiment and Cryptocurrency Risk Premia (2026)

NEW: R&R at Journal of Banking and Finance

(with Ilias Filippou and Ganesh Viswanath-Natraj)

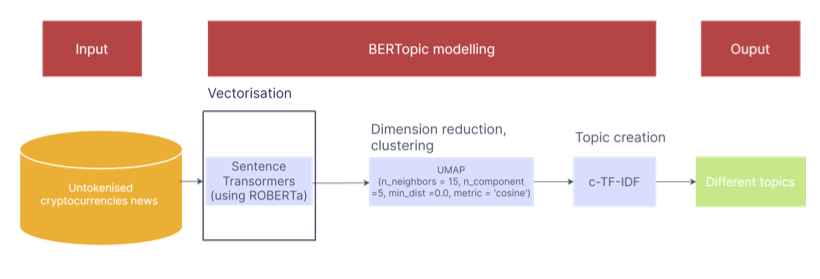

Abstract: This paper investigates the cross-sectional predictive ability of text-based factors in the cryptocurrency market –an important asset class for retail and institutional investors. We employ Bidirectional Encoder Representations from Transformers (BERT) topic modeling to analyze news articles discussing the top 43 cryptocurrencies by market capitalization. We build text-based factors related to fundamentals and technical trading. We find that technical sentiment is positively priced in the cross-section of crypto returns, while fundamental sentiment is negatively priced. These factors provide information over and above other factor models in the literature. Our results demonstrate the importance of considering text-based factors when analyzing cryptocurrency returns.

Presentations: Global AI Finance Research Conference (Ho Chi Minh City) 2023, INQUIRE* 2023 (London), Wolfe Research Annual Global Quantitative and Macro Investment Conference 2023 (New York), FMA 2023 (Chicago), MARBLE* 2023 (London), Gillmore Center for Financial Technology 2023.

2. The FOMC versus the Staff: Do Policymakers Add Value in Their Tales? (2023)

Federal Reserve Bank of Cleveland Working Paper WP 23-20

(with Ilias Filippou and James Mitchell)

Abstract: Using close to 40 years of textual data from FOMC transcripts and the Federal Reserve staff’s Greenbook/Tealbook, we extend Romer and Romer (2008) to test if the FOMC adds information relative to its staff forecasts not via its own quantitative forecasts but via its words. We use methods from natural language processing to extract from both types of document text-based forecasts that capture attentiveness to and sentiment about the macroeconomy. We test whether these text-based forecasts provide value-added in explaining the distribution of outcomes for GDP growth, the unemployment rate, and inflation. We find that FOMC tales about macroeconomic risks do add value in the tails, especially for GDP growth and the unemployment rate. For inflation, we find value-added in both FOMC point forecasts and narrative, once we extract from the text a broader set of measures of macroeconomic sentiment and risk attentiveness.

Presentations: Atlanta Fed* (2023), Cleveland Fed* (2023), New York Fed* (2019)

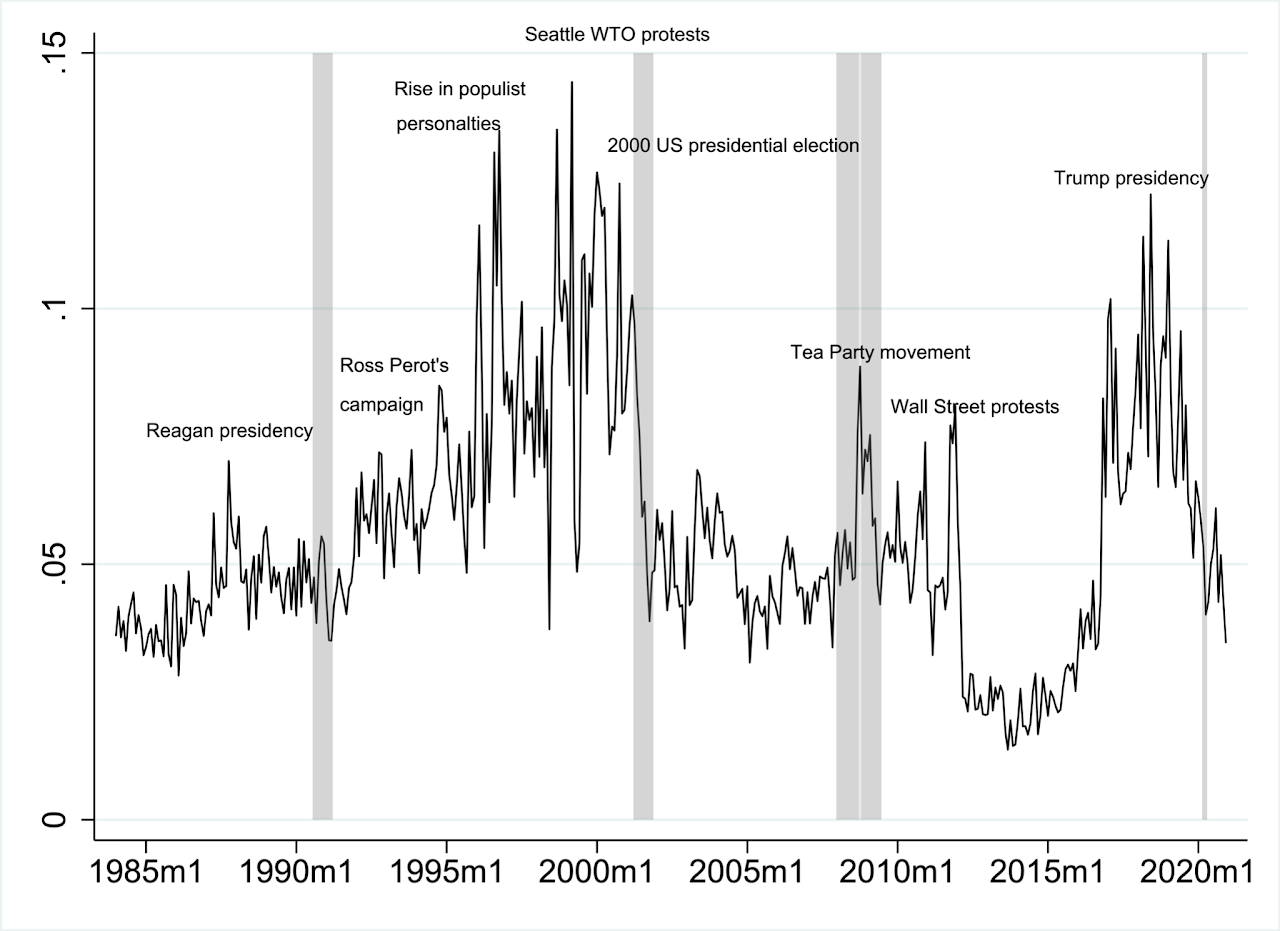

3. U.S. Populism and Currency Risk Premia (2023)

CEPR Discussion Paper No. DP15054

(with Ilias Filippou, Arie E. Gozluklu, and Mark P. Taylor)

Abstract: We develop a novel measure of U.S. populist rhetoric by extending an existing populist dictionary to capture the new form of populism via social media. Aggregate Populist Rhetoric (APR) Index spikes around well-known events that spur populist sentiment. We show that APR Index is priced in the cross-section of currency excess returns. Currencies that perform well (badly) when U.S. populist rhetoric is high yield low (high) expected excess returns. Investors require a risk premium for holding currencies that underperform in times of rising U.S. populist rhetoric. Centrality in a trade network partly explains our results and why friction to globalization in the form of populism affects the cross-section of currency returns.

Presentations: EFA* 2024 (Bratislava), RES* 2024 (Belfast), EEA* 2023 (Barcelona), FMA Applied Finance conference 2023 (New York), AFA 2021 (Chicago, Poster session), MFA* 2021 (Chicago), 2nd Frontiers of Factor Investing Conference 2021 (Lancaster), FMA 2020 (NY, virtual meeting).

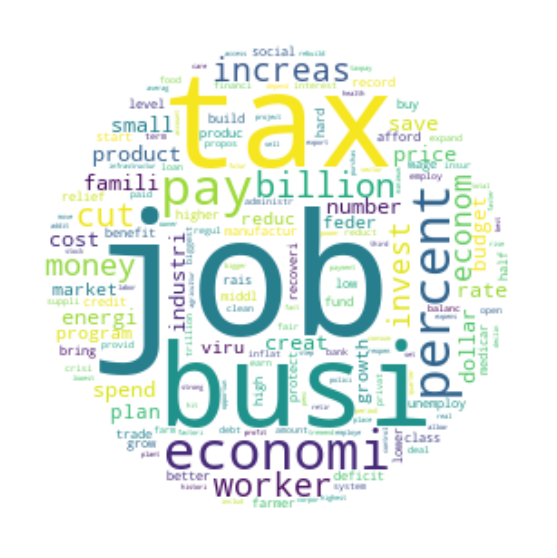

4. Text-based Fiscal News and the Cross-section of Stock Returns (2023)

Abstract: Using 9,524 speeches by U.S. presidents over the last century, this paper implements textual analysis to construct long time-series index for fiscal policy. The Fiscal News Index is a strong predictor in the cross-section of stock returns. Investors demand higher expected returns for holding stocks with high exposure to Fiscal News Index. The pricing implications of the Fiscal News Index are mainly through the discount rate news channel. Empirical results suggest that the Fiscal News Index outperforms other business cycle indicators in terms of pricing the cross-section of stock returns. The pricing implication of the Fiscal News Index is also reflected in currency returns.